Always late and behind the curve with my submission but I am a completer finisher so need a full set of reports even if they are late. This is just a quick summary of Q4 2021 and will leave the majority of the review and reflection to my end of year review.

Finance wise a good quarter with an average savings rate for the quarter of 64% (above my goal of 60%), total increase in net worth, £9,559 that is 5.7% increase since last quarter and 26% year to date.

Financial stress and the ongoing saga of the sale of a buy to let property was finally over 13 November 2021, yeahh, so now fully invested, more of this in my year in review.

Error Q4 Dec 22 should say Q4 Dec 21

Have done some great things this quarter including

Dino world at the Trafford Centre with my family including my great nephew

A visit to the Stoke Ceramic Biennale

Grayson’s Art Club at Manchester Art Gallery

A very long weekend in Amsterdam

Weekend with old college friends

Gigs including Baxter Dury and Tricky

Meal out with School friends

Walks around Cheesden Brook (2) and on the Millennium Walk Way New Mills

Bootcamp Xmas Do

Works Xmas Do at Tattu

An evening with Alan McGee

Xmas dinner with friends

More meals out with L and M

Family Xmas

Cream Tea at Hotel Gotham

Actions for last quarter

Complete my bootcamp 8 week plan and lose another 7lbs to include having a plan to get them abs

Completed but only 4lbs weight loss

Have a plan for if / when complete my R02

Complete fail

Complete the work on my flat, finally sell it and invest the money

Finally over the line and complete

Earning another £300-£400 in my side hustle

Actually earned £537

Think seriously about whether I will FIRE in June by 55th birthday. I need a pension valuation, another review, refresh and reflect on finances, and more importantly a real life plan of how I will spend my time.

It has been a good quarter personally and financially, socialy am getting out and about seeing friends and venturing back into the office one day a week. I would have killed to go into the office a few months ago but it all feels a little too much like hard work. I have also been focussing on getting fit and fit and training, community activities and my cat sitting side hustle

My studying for my second 20 CII credit module towards a qualification in personal finance R02 Investment Principles and Risk is still languishing by the wayside – I have refocussed my attention on training and community activities but it is still there as a possibility.

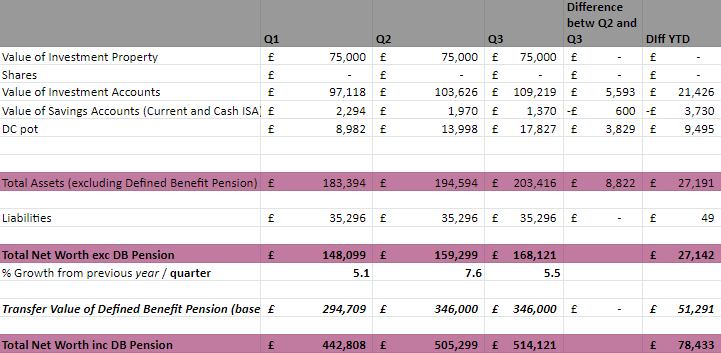

Finance wise a good quarter with an average savings rate for the quarter of xx (above my goal of 60%), total increase in net worth, £8,882 that is 5.5% increase since last quarter and 19.2% year to date. I took this data point right around 28/9 after which returns haven’t been so good!

MCR FIRE Meet ups had its first face to face meet up in August which was great, there was about 20 of us there at the height of the evening and a few of us stayed till throwing out time! We met online in July where two of our members Bertha and John told us ‘How they got started on their FI journey’ and September was not as advertised but we had an impromptu ‘FI Speed Dating Evening’ where members got to talk to other members about FI including ‘what is our worst investing mistake’ , ‘how do you engage our family in our FI journey’. We are now in a routine of one month face to face, next month online.

My main financial stress has been the ongoing saga of the sale of a buy to let property, it is still on tracks but what feels, like at times, not moving. As last month, some very expensive work needs doing as a condition of the sale. Everything is in place now with Planning Permission, Buildings Controls sorted and the work should start next week. So am really hoping it will all be done and dusted by Q4.

Have done some great things this quarter including

A long overdue visit to 2 old friends L and P

A 5 day cycle from Newcastle to Manchester

Walks with friends including A and LandS

A gin tasting evening with T, J and A

Organising a launch event and a craft trail for a small Pocket Park near me

Running guided walks as part of a local arts festival

Weekend visits to a friend in Peterborough and one to a friend in the Eden Valley

Actions from the last quarter / Q2

Complete my bootcamp 8 week plan and lose another 7lbs

Done and enjoyed it so much am doing it all again! I now have a new goal of getting some abs – am unsure how realistic it is!

Keep getting out in the outdoors including doing a 20mile walk along the Edale skyline

Done me and my friends had a lovely full days walking from Hope to Hope via Win Hill, Ringing Roger, Mam Tor, Hollings Cross….

Complete my learning for R02 and have my test booked in

Not done, lets bump that to next month

Complete the work on my flat, finally sell it and invest the money

Not done, lets bump that to next month

Earning another £300-£400 in my side hustle

Done, and some earned £719 side hustle income this quarter and while it won’t make me a millionaire, I really enjoy it, am cat sitting and it will really help with a few extra treats when I reach FI

Actions for next quarter

Complete my bootcamp 8 week plan and lose another 7lbs to include having a plan to get them abs

Have a plan for if / when complete my R02

Complete the work on my flat, finally sell it and invest the money

Earning another £300-£400 in my side hustle

Think seriously about whether I will FIRE in June by 55th birthday. I need a pension valuation, another review, refresh and reflect on finances, and more importantly a real life plan of how I will spend my time.

How was your Q3? Hope it went well and good luck with Q4, its nearly Xmas!

Q2 is going so well I missed posting my update and am over a month late. It’s a cliché but time flies while I am jogging along slowly. My horizons along with everyone else’s are opening up as restrictions are lifted, we can mingle, travel and socialise, more or less at our will.

It feels a different place that we are in compared to Jan-March – in terms of the pandemic, weather and a very much caveated sense of optimism and opening up – having enjoyed celebrations and the could have been moments of Euro 2020, the achievements of TeamGB in the Olympics, some great weather and the passing of spring into summer.

Have spent more time outdoors walking, running, cycling and have joined an outdoor boot camp which is quickly making me become obsessed with training and being ‘my best self’!

I have been doing quite a bit of community related activity, becoming more involved in a group to manage a community space near me and taking on the admin / co-ordinating role in some local litter picking activity (this may not be the glamorous life I had dreamed of)!

My studying for my second 20 CII credit module towards a qualification in personal finance R02 Investment Principles and Risk has fallen by the wayside unfortunately. I may need to prioritise or rethink my goals.

Finance wise a very good quarter with an average savings rate for the quarter of 63.5% (above my goal of 60%), total increase in net worth, £11,200 that is 7.1%. Am not sure I can keep this up as going out and holidays and a more normal life beckons but let’s see.

MCR FIRE Meet ups are going from strength to strength with ‘Investing in property – my thoughts after 10 years’ with Gary Derbridge, ‘Investing in the time of pandemic’ a conversation between Matt and Danny and ‘How much you need to be financially free’ from John B, April – June. Looking forward to the August meet up which is going to be our first face to face session since the pandemic!

Actions from Q1

Review my goals and make sure I am on track, particularly in terms of

increasing side hustle income

I am not on track with my ambitious goal of £3,000 but I have started – I registered ages ago with ‘Cat in a Flat’ a kitty sitting service, inspired by London FI meetup on side hustles. As restrictions lifted I got loads of enquiries and have already done 7 bookings, just finishing 2 more with 3 over the next few weeks. I have earned £410 so far.

read at least 1 book per month

I should have read 6 but I have only done 3, some catching up to do.

running – increasing frequency to 3 times per week and length of run to 50 mins

I am re thinking this goal. I have joined an outdoor boot camp and am going twice a week with other exercises and challenges – the goal of getting fitter and stronger is on track, but may be not by the planned route.

Sell the apartment and invest profits

This unfortunately has not happened, the sale is paused until some (very expensive for me) work has to be completed. It has at times being quite stressful and I just personally want it to end and have the money in an ISA or GIA. Hopefully next quarter will allow me to close this action down.

Review savings and investment direct debits

I did this, increasing my Pensions contributions and reducing, but only slightly my ISA contributions, to get to a 66% savings rate.

Pass my R02 exam

I’ve not done this, am reflecting on if this is where I want to spend my time – but as a completer finisher I think I will at least continue my learning and revising and take forward to Q3

Plan a cycling challenge with my friend

This was done and my friend T and I planned 5 day cycle from Newcastle, through County Durham, Richmond, Kettlewell, and Burnley and back to Manchester. We cycled this in the early July heatwave.

See friends face to face more regularly, go to the cinema and theatre

Has felt a busyish three months with

Meal out with J and B

Visit to Knutsford to meet N

2 walks in the South Pennines with J

Drinks and BBQ with J and A

A foraging day with A and T

A sunny week in Llandudno early June with my family

Celebrated my birthday with a garden party with lots of friends

Met with a group of friends to do a walk following the line of an ancient brook in South Manchester

Actions for next quarter

Complete my bootcamp 8 week plan and lose another 7lbs

Keep getting out in the outdoors including doing a 20mile walk along the Edale skyline

Complete my learning for R02 and have my test booked in

Complete the work on my flat, finally sell it and invest the money

Earning another £300-£400 in my side hustle

How was your Q2? Hope it went well and good luck with Q3, nearly half way through it already!

Another good quarter personally and financially. Professionally things as very much the same which veers from good to OK to please let this stop! With the not so startling conclusion that we are in this working from home for a good while yet I decided to create the ‘office of my dreams’, not quite but definitely make a concerted effort to create the best office I could. This involved tidying, a basic I know but something we can all be a bit lax on! A new paint job, new blinds, curtain to cover all the crap on my selves, blackboard paint and the piece de resistance two 24″ screen in addition to my laptop screen. While not quite Minority Report, something I am definitely bragging about.

The transformation of my working space has made the space so much nicer to be in and while it is still my ‘work’ environment I enjoy being in it. I did ask myself why did I not invest the time and money earlier (all in all it cost around £500 for screens, stand and decorating and furnishings. and maybe a week of my time).

I work in change management so it is ironic that I have been hoping for things to go back to how they were rather than accepting how they are and taking steps to integrate this new way of working effectively into my life. The change curve is a well known model or framework to understand how we as individuals engage with change, it simplifies things of course and our journey is not always as linear as the diagram suggests with lots of too-ing and fro-ing. However it does describe the processes I have been going through moving from low mood to exploring solutions and accepting the need to spend some time and a bit of money to improve my work environment. And now according to the model am apparently moving forward and accepting this can work for me and even be good for me! Let’s see.

Reviewing previous posts Q1 2021 it has been a much quieter three months, winter shrinking still further the already limiting effects of the pandemic restrictions. However I am still connecting regularly with family and friends, face to face and online and getting out walking, running and cycling.

Another big fat tick personally has been finally passing R01 Financial services, regulation and ethics, a 20 CII credit module towards a qualification in personal finance back in February. It was a huge confidence boost to pass it, and pass it well as I had struggled with the content. I do not work in financial services and had to spend much much more than the recommended study hours. Now on to R02 Investment Principles and Risk which already I am finding much more interesting, but just as challenging.

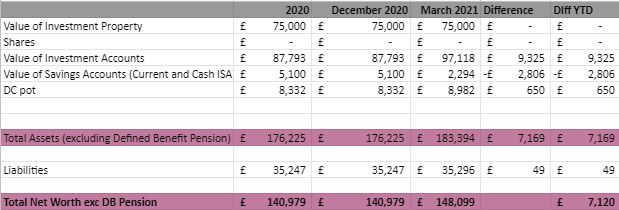

Finance wise a good quarter with an average savings rate for the quarter of 59% (1% less than my goal of 60%), total increase in net worth, £7,169, that is 5.1%.

Actions from last quarter

Last quarter my goals were to pass my R01 exam, which I did do and to start match betting, again which I did do but immediately stopped. I really didn’t fully explore it but it just didn’t feel comfortable. While I am ok with numbers I am not agile and need time and on a Saturday morning I just didn’t want to do it. I felt put off – I think I did have a slight hang over as well, not sure if that had an impact?! Anyway have dipped my toe in the water and may go back, but lets see!

I also participated n ChooseFIx courtesy of an introduction by JK, which was about testing a model of building a community around FI and personal development. The activity is on pause while the ChooseFIx team are taking on feedback and developing the next step. The key activity I enjoyed was goal setting and participating in a health reset which resulted in me losing 16lbs, getting back into cooking and being carb free for 2 months. I have not progressed as well with either my side hustle goal of earning £3,000 this year (see above for my aborted attempts at match betting) or my reading goals, one book a month.

We are still in the process of selling our flat as the buyers sale fell through and they had to go back to square one. We are looking at a 1/5 completion date. I will then invest the money in my S&S ISA and a GIA and redirect all the money I would have put in my ISA into my pension.

The FIRE Meetups are going really well with one per month. And we now how events diarised until September, which a face to face event in August, all going well. This last quarter we covered

Being the change – using financial independence to improve the workplace

Let’s talk about the Savings Rate

Finding your way in Finance – Pensions vs ISAs

After ‘Finding your way in Finance – Pensions vs ISAs’ I decided to divert money from my ISA to pensions and invested an additional £2,000 into my ISA from savings. Another financial achievement – nearly maxing out my ISA allowance for the first year ever (£700 spare). I have also had my first vaccination and looking forward to May for my second.

Actions for Q2 2021

Review my goals and make sure I am on track, particularly in terms of

increasing side hustle income

read at least 1 book per month

running – increasing frequency to 3 times per week and length of run to 50 mins

Sell the apartment and invest profits

Review savings and investment direct debits to

Pass my R02 exam

Plan a cycling challenge with my friend

See friends face to face more regularly, go to the cinema and theatre

So how was your last quarter of the year? Hope it went well and good luck with Q2.

I have loved reading Indeedably’s Sovereign Quest challenge ‘Planning for Decumulation‘, including Weenie, FI UK Money and Gentlemen’s Family Finance. I may be a bit late to the party but thought I would put my two penneth in. It has been an interesting to contemplate and work out some of the detail.

Until thinking about this challenge I was like Weenie – I had a high level plan that has some shape to it, but the nitty gritty was, and still is to some extent, less sure about. Am hoping to use this post to flesh out some of that detail and would love to get some views.

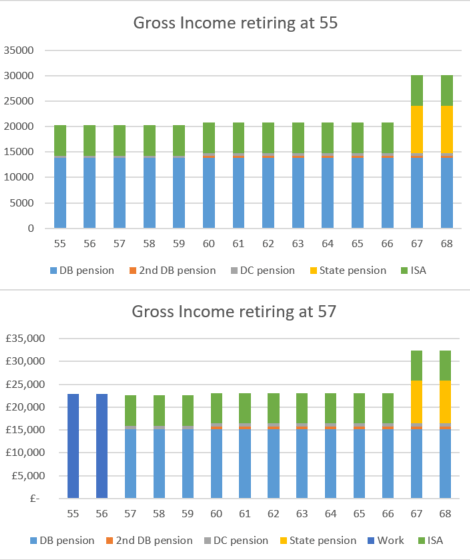

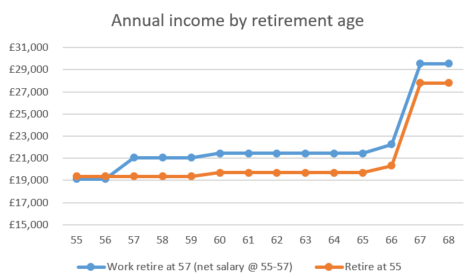

On paper I could FIRE in a year at aged 55 but I am considering working a couple of years as a) I’d like that little bit more annual income those two years could give me b) I don’t hate my job and c) I could have the opportunity to work part time. Anyway for the purpose of this post I have compared two options

Leave work and take my DB pension at 55

Continue working full time and take my DB pension at 57

And am assuming working part-time will give me somewhere in the middle. As I said I don’t mind my job, I like it and my colleagues – it’s just the doing it every day thing that bothers me!

I think my situation is relatively simple as a key part of my plan is a DB pension which I can take at 55 so I don’t have to worry too much about running out. Also to clarify to increase my DB pension I will be taking 0 tax free lump sum.

Assumptions

I am married but I do my FIRE journey and calculations just for me, not as a couple. My assumptions are that my partner will carry on working and earning until the state retirement age, currently 67 for us. They will then have a state pension with a goal (mine not necessarily their’s!) of about of £150,000 in a SIPP.

It is possible we will both inherit some money in the tens of thousands but this is not included in any of our calculations.

Other assumptions

4% withdrawal rate for DC pension and ISA

All current tax rules

The pension modeller provided by work is correct

State pension

I include the State Pension in my figures because a) it doesn’t work unless I do! and b) because of my age and c) because I cannot see any party having the political will to challenge a universal state pension based on contribution in favour of means testing. I cannot envision a world in which a government runs an election campaign which says ‘you know that state pension all previous generations have had and you are paying the National Insurance Contributions toward – well it won’t be there for you, in fact – if you work hard and save toward retirement we’ll just take it off you pound for pound’.

Both of which are definitely viable, but not means testing, in my view.

What type of life do I want?

I am making sure I continue building my talent stack at work as I may want to or need to work beyond 57 to have the type of life I plan for.

I will want to extensively travel so that will need funding, though when travelling I am happy to stay in hostel type accommodation, get buses and trains and manage bookings myself which all keeps cost down. I also love doing walking and cycling holidays close to home so again that can help manage costs.

All things I love doing are relatively low cost, running, cycling, walking, socialising, cinema a bit of theatre and art galleries – I can cut my cloth to fit if needs be and do not have many expensive habits.

Behavioural

I do enjoy the daily interaction with people that a job brings, but I think I can through social networks, working and volunteering emulate that in my post work FI lifestyle.

I also have a couple of work / study / career change options I am exploring so who knows. I also have hobbies and things I like doing and would like to do more of so am thinking having time on my hands will not phase me. My parents are getting older and I do want to spend more time with them. Even though we all know none of us live for ever, to be faced with the fact our time together is limited makes me think I want to be there for them if they need me to care for them.

Legacy

I am child free and whereas I love my nephews and my great nephew I am not planning on leaving them lots of money, but if I do it is split 50/50 between people and charities.

The figures

So looking at my figures, the majority of my post FI lifestyle will be funded by DB pension, topped up with my ISA investments, a thin sliver of a small DC pot and an even smaller second DB pot (available from aged 60) from my first job after A Levels – and the State Pension from 67.

Whether I retire at 55 or 57 up to state retirement age about two thirds of my gross income will be from by DB pension, between 2-3% from my DC pension and a third from my ISA. So two thirds of my income will be index linked free of volatility worry.

What I have worked out is that my FI net income is more than my net current income! (i.e. my living and discretionary spends, not including my savings and investments), by just £150 if I retired at 55 but by nearly £2,000 net if I work the extra 2 years and continue with the same level of savings and investments.

I had never done this specific calculation before so it has been really illuminating and brings me comfort.

Also if I work for another two years I will have around £1,700 more per month, with a total net income of around £21,000. And this feels alright, well more than alright, it means I am not lean, but not fat.

According to the Retirement Living Standards this is a Moderate income for an individual and is two thirds of a couple’s Moderate income. So as a household it is indicating to me that we will be fine as my partner will carry on working until 67 and then we both will get State Pension which may, with the wind in the right direction, get us to Comfortable for a couple standard of living.

It has taken quite a bit of work to get down to the last pound and penny on these calculations but even though I am between 1-3 years of hitting FI, things can change with numbers, I do need to get the pension numbers validated and just doing this exercise has me changing my plans!

Also as a result of the MCR FIRE meet up session on Friday March 19 with Indy, a Financial Advisor, I have been challenging myself as to why I am putting so much in my Stocks & Shares ISA and am not taking more advantage of the DC scheme available through my work (in addition to the DB scheme). Indy also has made me think about the role of the tax free 25% of the DC pension in my planning. So no sooner have I written this than I am changing my accumulation principles – however the idea is that the numbers will be similar, if not better but the S&S ISA plays a less significant role.

It has taken me a while to do this post but have enjoyed it. I think I know my numbers but being more forensic about it has given me a lot more clarity, plus it has, along with the MCR FIRE meet up session, made me reflect on my accumulation strategy.

I would definitely encourage people to do this. Am also interested in any thoughts anyone has on what I could improve on.

I had to get this in before the end of January as you can’t do a year in review once we are February. It’s the rules!

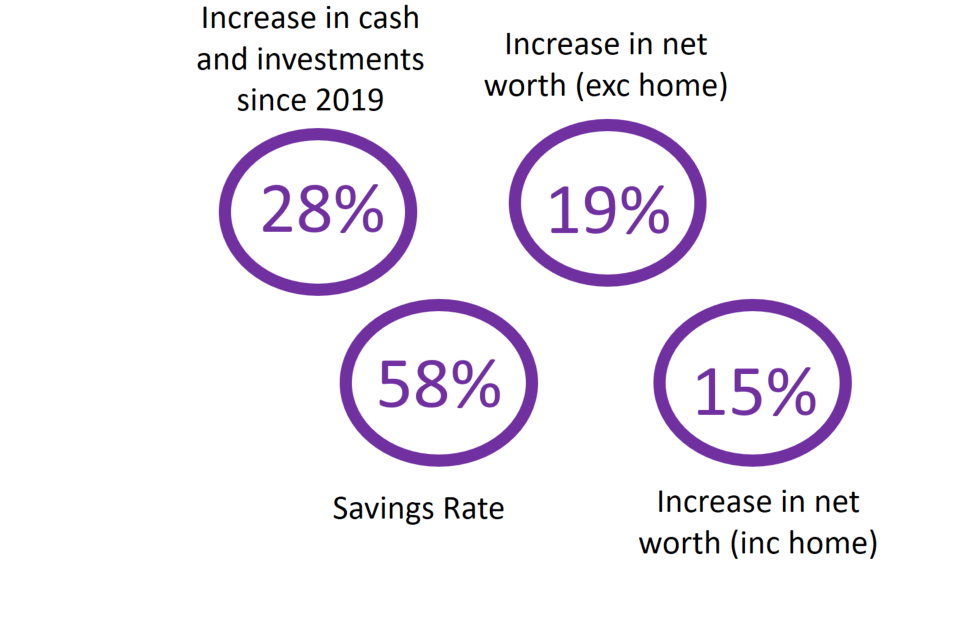

2020 was another good year financially. I remained fully employed working at home, with limited discretionary expenditure on going out and holidays allowing me to increase my savings rate. I like to measure

Increase in cash and investments

Increase in net worth (exc home)

Increase in net worth (inc home)

Savings rate

Some good numbers comparing last year. I have either maintained the number or increased it everywhere except ‘Increase in net (exc home)’. I think this is because last year our buy-to-let property was revalued so had a bit of a jump for that category. A big increase in Savings Rate so was hoping for a bit more on ‘Increase in cash and investments’ but obviously the numbers are getting bigger making it harder to increase the percentage. Most of the increase is through investing rather than capital growth.

Increase in net worth (inc home) shot up as my neighbours sold their house last year giving me a reliable revaluation.

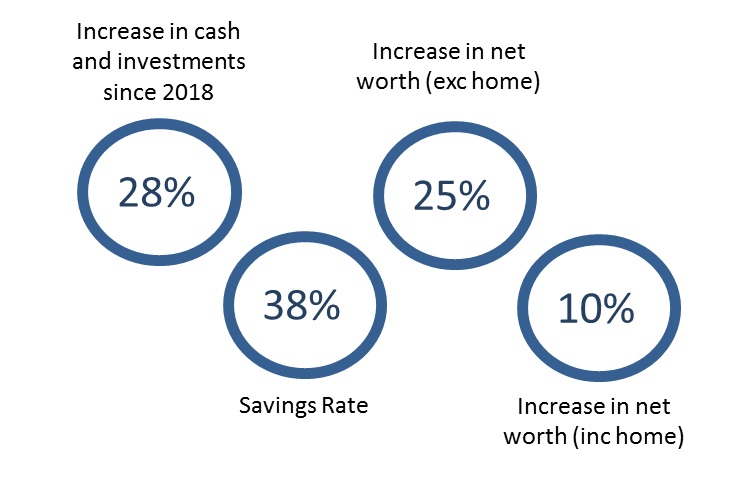

My Financial Year in Numbers in 2020

and for comparison…

…. 2019

Last year I was boasting I had got into good habits in 2019 in terms of increasing % of savings in investments and decreasing the % of my total net worth in cash – I was delusional. This year I nailed it by moving all cash except £5,000 in premium bonds into investments. I also decided with my partner to sell the buy-to-let we have, realise the cash and invest and forget. My 2020 goals were

Financial

Increase savings rate to 40%

nearly there at 38% but could have done better, but I was using gross income as a measure and have change to net income so am fudging my figures a bit !

Increase in net worth to exceed or at least be in line with 2019 figures i.e. 28% increase in net worth

done

Increase savings / income by £2,000 with side hustles / squirreling / being more ruthless with budgeting

done easily through not having to be that ruthless with budgeting, just nothing to spend our money on due to Covid-19. I did manage some side hustle income to around £900 with the rest and more being made up of extra money due to Covid-19 restrictions.

The full suite of squirrel pots to manage all my current and projected expenditure including living expenses, discretionary expenses, holiday, DIY fund and Xmas expenditure are doing a great job.

Focus on well-being and get a better better work / life balance, leave work on time, sleep better and don’t self medicate – which will leave me more time, energy and head space to do more of the things that make me happy

This is all a bit of a blur, I am not sure I did achieve this at all. Work bleeding into life, life bleeding into work, lots of cheap cider, very little energy and head space unfortunately. Someone at work had a good phrase for this blurring of our work and home lives, ‘I am not working at home I am living at work’. This did improve as the year went on but this is something that needs attention in 2021.

Preparation for FI

As well as all the the financial goals above, I also want to work on getting myself and my partner ‘on the same page

Oh this makes me laugh, this definitely did not go to plan, we are still very different, am working on it, but it will not be resolved any time in 2021.

I have also upped my reading of FI books, am not a great reader any more but worked my way through, Your money or your life, Simple Path to Wealth, Financial Freedom and RESET. I also took some free financial online courses as well as registered for the Award in Financial Services, signed up to take the initial module R01 – Financial Services, Regulation and Ethics with the aim of taking the exam in February 2021.

Have been participating in ChooseFIx – a community to develop and grow personally as well as part of my journey to FI. The first activity we did as a group was goal setting using the principles of Dominick Quartuccio – listen to him on the ChooseFI podcast.

As a result I have loads of goals, but the main ones are

Financial

Have a consistent savings rate of 60% with one month at 70%

Give monthly to charity

Raise £500 for charity

Earn £3,000 in side hustle income

Learning and work

Achieve award in Financial Services. Produce Research proposal for a PhD in FIRE

Take the qualifications to be a a Senior Project Manager

Health, self, friends and family

Look after myself, ensuring I have a good nights sleep, have a good work life balance and don’t drink to much

Loose 10lbs

Run three times a week and do a half marathon

Read a book a month

Connect with family and friends weekly

Good luck with your goals and keep safe and well in 2021.

A good quarterly personally, professionally and financially. I find as the end of the year comes into view I accelerate on things that have been outstanding for while with renewed vigour. I finished work on 18 December with a relatively tidy inbox, almost completed to do list and some good feedback from colleagues on my work last year.

I made some good progress until mid December on the R01 Financial services, regulation and ethics 20 CII credits towards a qualification in personal finance. The goal for taking the exam was end of November but I had mentally moved it to early January. Now having had 2 weeks off over Xmas it is on the move again to end of January.

I have found the study difficult, it is all new concepts and terminology to me. The knowledge is not ‘sticky’ I do not work in financial services so I have to learn by rote – I have limited personal experience on to which I can hang this new knowledge. I have to immerse myself in the content, study it more or less every day and maintain momentum to be successful – and Xmas has got in the way. Back on the wagon in January !

Finance wise what a great quarter with an average savings rate of 57.5%, total increase in net worth, and I can’t believe it and have to check it as I am typing it, of £10,185, that is 7.8%. These numbers have me doubting my spreadsheet, but it is true!.

With 18.7% YTD increase in net worth.

Last quarter I had committed to addressing my financial biases of hold onto assets for emotional rather than financial reasons. The three actions I took to address this bias are below and I am pleased that these have moving forward at a pace

sell the Royal Mail Shares I have seen rise then plummet since 2013, and invest in tracker funds

I did this back in October and disappointedly I sold them at a loss and they are now back to price i bought them – this is an exercise in learning to letting go!

transfer c£11k held in a cash ISA to a Stocks and Shares ISA, so I am fully invested

Done and enjoying my new simplified spreadsheet. Am also becoming a bit of a fully invested bore giving my family and friends the benefit of my insight – not sure am making much of a dent yet but am keeping going

made the decision to sell our buy to let apartment. It will be difficult emotionally to let go. It has not been a terrible investment financially but financially and hassle wise it doesn’t quite stack up as nicely as invest and forget!

An offer was in within 2-3 weeks of it going on sale and looking at completion by the end of January 2021.

I did some great things this last quarter

Three fantastic MCR FIRE meet ups covering Hacking your 9-5, Logan Leckie talking about his new FI app and a session from our good friends in London on Side Hustle Challenges

The London FIRE meet up on personal finance

A few meals out before we went into the second lockdown

Lightopia in Heaton Park North Manchester

Roaming wine club – which involved walking around a local beauty spot with friends and wine

Al fresco drinking with friends. Now pubs and bars are shut I have been enjoying, cider by the river, beer in the Northern Quarter and drinks on park benches with friends as well as a Christmas Eve on deck chairs on a bit of green near my house

Lovely Xmas masked and distanced get together with family

Walks around South Manchester and Jumbles Reservoir in Bolton

Actions from last quarter

I did indeed pull my finger out and knuckled down to studying for my 20 CII credits Financial services, regulation and ethics module – but as above not quite in the position of finishing this calendar year with one module under my belt. And I still have not carved out some time to take full advantage of the help SA gave us at the August FIRE meet-up demystifying Match Betting. Lots to do in 2021.

I also got involved in ChooseFIx courtesy of an introduction by JK, which is all about building a community around FI and personal development, being 1% better each day and having accountability to support us meeting or FI and personal goals. We are just getting started with our 2021 goals, will let you know how we get on.

Actions for Q1 2021

Develop my 2021 goals

Deliver actions to meet my goals

Sell the apartment and invest profits

Pass my R01 exam

Register for the Pensions module for the Award in Financial Services

Set up 3-4 MCR FIRE meet ups

So how was your last quarter of the year, what was your experience of the markets and did your net worth get a nice boost? Do you set goals, what is your process and are you being ambitious for 2021?

Many of my colleagues are enjoying working from home using those extra commuting hours to exercise, spend more time with their family or just enjoying the extra free time. Not me. The lines between home and work are blurred and my working day is expanding. Some of things I would like to do in my spare time, such as blogging, I just can’t seem to find the time or more usually I just do not want to spend any more time on the computer. So this is now a quarterly and not a monthly update!

I am still working from home 100% of the time and finding I am actually quite enjoying ‘some’ things about it, in particular fitting in domestic chores (sad I know) and getting up later. But I waiver between exhausted and tired. Working at home, focussing on a computer screen and meeting via Zoom is draining without the variety and activity a day in the office brings. I miss my colleagues. At the start of lockdown we all amazed ourselves how quickly we managed to shift gear to working online realising lots of benefits of remote working. Now 6 months on the gaps and difficulties are more visible, largely for me around the informal and social aspect of work which oils the wheels of how we get things done as well as being genuinely enjoyable, the quick catch ups where things can be moved on quickly or you pick up important details about a change or a project. But here we are and here we will stay as infection rates increase and there is talk of increased restrictions in the north.

I still have a poster I created above my computer ‘I am not my job’ inspired by Vicki Robin and Jo Dominguez in ‘Your Money or Your Life’ reminding me not to link what drives and interests me with how I earn my money. It sounds like I don’t like my job, I do, I just doing like all of it all of the time!

Finance wise its a bit of a mixed bag in terms of net worth increase but I am continuing with a really good savings rate. Even in September when we had a week away in London, Brighton and Kent and a long weekend in the Eden Valley I still managed 53%. In summary

Month / Savings Rate / Net worth Increase £ / Net worth Increase %

July / 62% / £703 / 0.6%

August / 59% / £3654 / 3%

September / 53% / £701 / 0.6%

With 10% YTD increase in net worth.

Also financially I know I have my biases – I tend to hold onto assets for emotional rather than financial reasons. My biases were confirmed by the ‘Beam app‘ which assesses your biases for borrowing and investing. It is super interesting and engaging app. I apparently have a very high ‘endowment effect’, which causes me to inflate the value of an object, simply because I own it, a typical ‘confirmation bias’, which is the tendency to favour information that confirms my existing belief and a ‘high probability neglect’, which describes my tendency to disregard probability when making decisions. I am hoping, time permitting to do a future post on the app.

Anyway the three actions I have taken to be more rationale in my financial behaviour

sell the Royal Mail Shares I have seen rise then plummet since 2013, and invest in tracker funds

transfer c£11k held in a cash ISA to a Stocks and Shares ISA, so I am fully invested

made the decision to sell our buy to let apartment. It will be difficult emotionally to let go. It has not been a terrible investment financially but financially and hassle wise it doesn’t quite stack up as nicely as invest and forget!

Actions from July

I finally finished Grant Sabatier’s ‘Financial Freedom’ where he describes his journey from 0 to over £1 million in 5-6 years, becoming financially independent by the time he was thirty. Key takeaways were about earning more money through side hustles – he really focussed on increasing his income by both using his 9-5 skills of digital marketing to pick up his own clients and more usual side hustles such as cat sitting ! He took any and every opportunity to make, and then invest more money. A very inspiring read. Am also nearly at the end of David Sawyer’s RESET, a great actionable book which has motivated me to do some digital and physical streamlining as well as making me feel comfortable with my current investment strategy of Vanguard Life Strategy funds. But he also describes a number of different portfolio options which, if I get bored of invest and forget, I might consider!

I also completed a free Open Learn OU course ‘Managing My Financial Journey‘, about the history of the banking and finance industry, causes of the Great Financial Crash and how it changed Financial Services, Financial Regulation and financial products. It has helped a bit in providing some foundation knowledge to (R01) Financial services, regulation and ethics 20 CII credits. I finally signed up for the ‘Award in Financial Administration’ and started all enthusiastic, but have been a bit on the back foot since I returned from holiday earlier in September. It is very detailed and some of it is very boring! But I am committed to taking the exam hopefully in November then review how I feel taking the next module (FA2) Pensions administration 10 CII credits.

I did some great things this last month

A Manchester FIRE meet up – with SA giving us a fantastic intro and overview of Match Betting

The London FIRE meet up

Week in Brighton, Kent and London

Long weekend in the Eden Valley

Cocktails, eating out and cinema

Cycling the Cheshire Ring

My first hair cut since lockdown

Its all feeling a bit more normal.

I also celebrated two anniversaries. My first year blogging and a full year of being involved in MCR FIRE meet-ups which are going from strength to strength. Our next meet up is ‘Hack your 9-5‘ 23 October.

Action for next month

I need to pull my finger out and do my 20 CII credits Financial services, regulation and ethics module to make sure I can finish this calendar year with one module under my belt. I also want to carve out some time to take full advantage of the help Siu Ann gave us at the August FIRE meet-up demystifying Match Betting and give it a go.

I’ve also got to prep for our next MCR meet up ‘Hack your 9-5‘ on 23 October.

So how has your net worth faired these last few months? How are you managing lock down? Has your routine changed much? What are you financial biases and have you made any behavioural changes?

June has been a much better month for me, I have felt less stressed and anxious, had a birthday and done some really nice virtual and face to face social activities.

I am making sure I keep track of my well being and do something every day which I know makes me feel better. I have also taken the advice of Vicki Robin and Jo Dominguez in ‘Your Money or Your Life’ and not linked ‘work’ and what drive and interests me with how I earn my money.

Again as last month due to a reduced monthly expenditure I am able to save an additional amount, less than last month but still £380. This boosts me to a 61% savings rate for June. The goal is for increasing my savings rate to be some kind of weird kick and something I am motivated to keep going as restrictions are released.

In terms of net worth June is another bumper month from my point of view with an increase of £3,532 from last month increasing the YTD increase to 5.9%.

How odd does it feel with such a strong bounce back by the stock market at the same time as any companies starting to announce redundancies?

Actions from June

Last month I have been continuing my financial education. I did put together a ‘Transformation Plan’ which outlines what I need to do over the next 2 years to change my career to Financial Services. A ‘Transformation Plan‘ is a really useful and visual tool to show what activities you need to achieve over time to realise your goal or vision.

It was also the June MCR FIRE meet-up online – FI Book Club on 19 June where I introduced ‘Your Money or Your Life’ by Vicki Robin and Jo Dominguez and C gave us a summary of ‘The Millionaire Next Door’. As usual a really good evening chatting with like-minded people. The next meet up is in August with a focus on side hustles, in particular Match Betting which am very interested in.

Personal Expenditure last month

Total personal expenditure for June £380, again an increase on the previous month from 38% to 49% of what I actually allocate. Again largest categories Charity and ‘Entertainment’. Quite a bit on presents as had some birthdays but also unfortunately some lovely colleagues leaving my work for other jobs and leaving fixed term contracts. As restrictions are released I had my first trip back on public transport and a trip into town for a meal out. Felt strange and strangely familiar .

I did some great things this month

A virtual cocktail night with ex and current work colleagues

A face to face wine club meet up with friends

A picnic in the rain for my birthday!

The London FIRE meet up

Action for next month

I am half way through Grant Sabatier’s ‘Financial Freedom’. I am finding I am enjoying reading FI books rather than blogs at the minute. I find reading a book requires more concentration – so it makes me focus, and its not on screen so its suiting me more at the minute. I am also half way through a free Open Learn OU course ‘Managing My Financial Journey‘, which isn’t really about managing your financial journey it is about the history of the banking and finance industry, causes of the Great Financial Crash and how it changed Financial Services, Financial Regulation and financial products. Sounds boring but its not am enjoying it and I am hoping it will help with my studies toward a career change to Financial Services.

So my priority is to finish ‘Financial Freedom’ and the OU course and sign up for the Chartered Insurance Institute ‘Award in Financial Administration’, and get started proper with getting some financial qualifications under my belt.

I spoke a little too soon about being on an even keel with working and living at home more. May has felt a real rollercoaster mentally. I have felt stressed and anxious, to the extent I have had to take a ½ day leave. Fortunately, my line manager and colleagues are caring and supportive people thatI can talk to about how I feel and try to understand the help I need.

I think many of us know what we should be doing to improve our mental wellbeing, and on the face of it, they are very simple things. Simple, but not easy. Get enough sleep, meditate, reduce alcohol, exercise, do more of what bring you joy, take regular breaks… breathe deeply etc. Like financial wellbeing it is about building good habits and automating as much as you can.

So how can I use how what works for me in my financial wellbeing to help my mental wellbeing? Part of what works for me is tracking and following the process. Deciding ‘this is what I will do’, track I have done it, and measure the results. I saw a great simple little chart flash by me on Facebook ….

It doesn’t matter what the categories are, meditate or go for a walk, read one chapter of a book or listen to a podcast, it is just about each of us identifying the things we know are good for us or that we like doing. Then commit to doing at least one or two of these a day and make sure we do each one at least once a week.

I think the root cause of my stress is not having the face to face interaction really enjoy about work. Separating work from the place and people makes me question the value and meaning of the work – but I will have to try and understand and manage it as I think it will be a few months before we will be able to return to the office and even then it may not be full-time.

Many bloggers have been very busy during lockdown, but I am still behind with both reading and writing, but what has been clear is that many of us have seen an increase in monthly net worth figures.

Since last month I have decided to give my savings rate a boost by using my net rather than gross income – which has meant an increase from 40% to 50% – just like that! Also due to a reduced monthly expenditure I was able to save an additional £463 which boosts me to a 63% savings rate for May.

My net worth has seen an increase of lovely £5,076 or 4.3% from last month (huge yeah), and up 2.9% from the end of 2019. What a difference a month makes. But we are in it for the long haul and we just don’t know what is around the corner.

Actions from April

This month I wanted to concentrate on my financial education – have progressed with completing ‘The Simple Path the Wealth’ and a good way through ‘Your Money or Your Life’. More still to read with the Choose FI book and David Sawyer’s RESET still on my to read list, and have ordered Dave Ramsey’s Total Money’s Make Over.

I completed FI101 ChooseFI’s online FI course. Can’t recommend this enough, a really clear, engaging course that takes you through their ‘blueprint for FI’, it uses text and video to explain concepts, has activities to work through and links to supporting resources. I would like to do a full review of the course as it is worth promoting.

As part of being my work team’s ‘wellbeing champion’, I saw a gap in the wellbeing resources provided by my workplace – nothing on financial wellbeing directly though they do do a pre-retirement course – so I have drafted a session I am planning on offering to my colleagues.

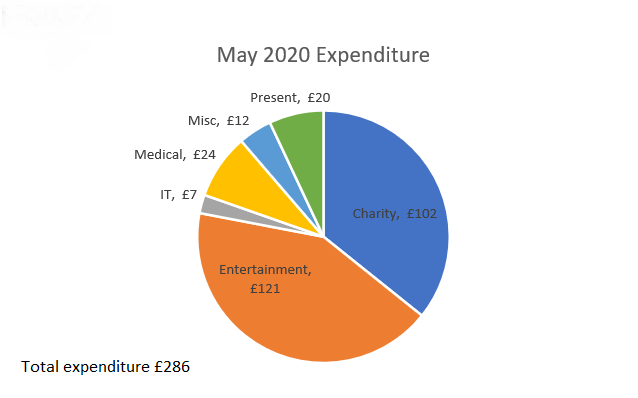

Personal Expenditure last month

Total personal expenditure for May £286, an increase from last month but still 38% of what I actually allocate. Largest categories Charity and ‘Entertainment’ which now consists of books, posh take outs and booze. I did spend some accrued underspend from previous months on a lovely iPhone 11.

Action for next month

Next month am continuing with my financial education, reading etc and also, I am putting a plan together to, at some point over the next 2-4 years, when I reach FI, change career to something in Financial Services. To this end I have set up a Facebook group for likeminded people to share their journeys on ‘Becoming a Financial Advisor’. Join us if you are interested. I am also exploring other avenues of financial coaching and researching FIRE.

It’s also the June MCR FIRE meet-up online – FI Book Club on 19 June via Zoom. If you’ve read books come and share or come along and pick up some tips for some good reads.

{kind=link}