I’ve been using ‘pots’ for years now to earmark funds for specific purposes. I started off simple, just the one or two pots. My oldest pot is ‘monthly spends’ a slush fund for discretionary expenses; booze, cinema, trips out… all that good stuff.

My pots are usually virtual rather than physical; current, savings accounts etc. But I have used physical pots (actually an empty tin of Uncle Jo’s mint balls) to squirrel money away.

Dave Ramsey talks like he invented potting (my snideness hides huge fandom, the subject of a future post), but calls it ‘The envelope system‘, having an envelope for each budget category, usually discretionary categories that it is easy to over spend on e.g. groceries, or going-out. Cash is put in each envelope so you ear mark your spending for that category – and his rules are, no money in the envelope no money to spend.

Putting a virtual or physical ring fence around funds for different spending categories is so simple but so powerful.

It allows you to see your progress toward specific goals.

It creates enforced scarcity so you don’t over spend.

It provides focus – a specificity which which drives good behaviour e.g. more intentional spending or increasing the drive to save.

It makes measurement simpler, and we all know what happens when you measure.

It provides transparency and clarity about what is happening to your money, where its going, showing either your priorities or your excesses.

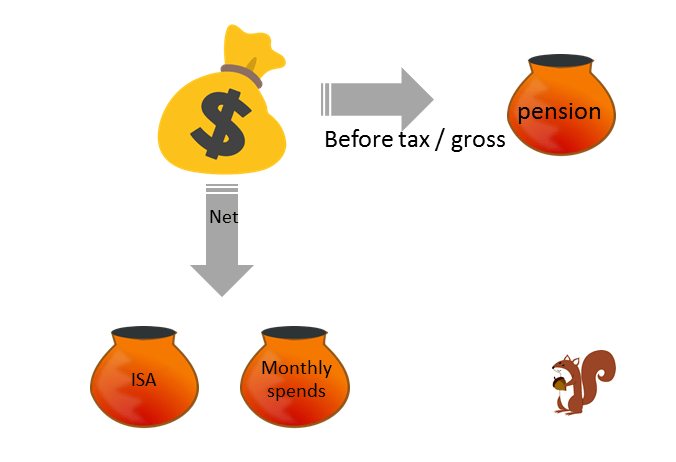

Level 1 potting

It must be over 20 years since I started potting – this level one potting was mainly for my monthly spends as well as a pension and stocks and shares ISA pot.

I have always found separating off my monthly spending, all that lovely fun stuff that can just have your money disappearing into a round here and a lunch there, a corner stone of managing my money. This is the only account I have and do sometimes use an overdraft on. Even though I do have money elsewhere I would not use it for my monthly spends, opting instead to go into overdraft, suffer a fee and have to recoup the money from the next month.

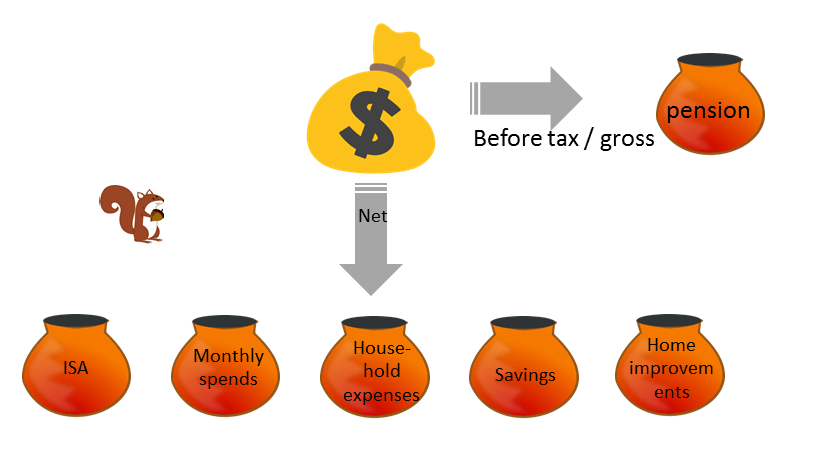

Level 2 potting

When I really started getting intentional with my spending, and it may have coincided with my partner and I getting married and joining our finances, I can’t quite remember, but I took the potting up a level! Pots for household expenses, savings and home improvements were born. Like monthly spends household expenses is another cornerstone of managing expenditure. I kick myself that it took so long to get it set up. My finances were stabilising and my income increasing enabling me to save and think ahead on how to finance significant activity such as home improvements. This pot has allowed me to finance some very expensive but absolutely gorgeous sash windows!

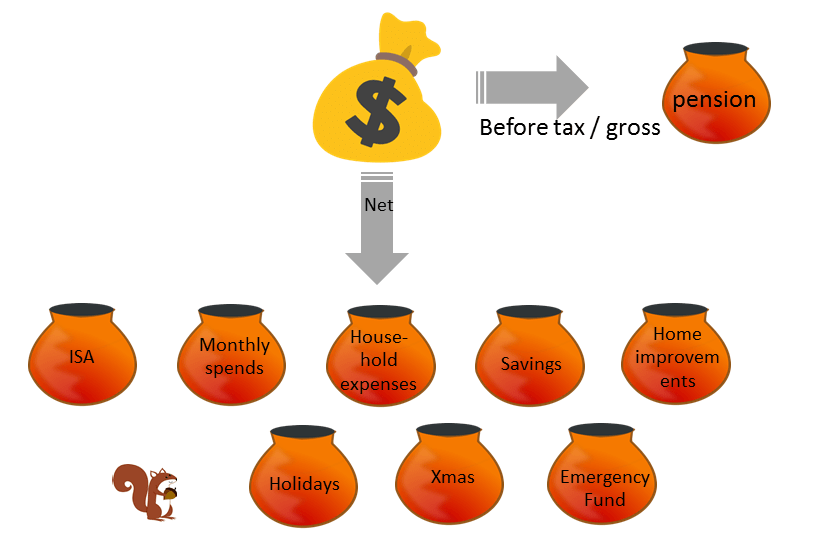

Level 3 potting

I have now reached potting nirvana – a full set of pots where every pound is accounted for. This is a very recent state of financial affairs. I listen to Dave Ramsey on loop and he prescribes the every dollar budget where every single dollar is accounted for. With level 2 potting there was money hanging around, some of it I classed as an emergency fund, some of it I used for holidays or propping up other pots, basically it was a a bit sloppy and ill disciplined. So I set up two new pots, holidays and Xmas. I have set up an account with a local credit union for Xmas spends to support community based ethical saving and lending. I also decided to define more clearly my emergency fund and inspired by Maven Money podcast (espisode 142) have put £5,000 emergency fund into Premium Bonds.

Now ever pound is accounted for so I can now track my priorities and my excesses!

Are you a potter? Are you Level 1, 2 or 3?

I don’t use pots to plan spending nut I do categorise my spending like this.

I suppose that having a budget and sticking to it really helps especially when there is no shortage of things to spend money on.

I have bent my own rules for car purchases – if you buy a car do you put that down as £Xk spending for.one month and I spent £3000 last month on our windows – that should be a spend that will last 20 years but it.makes January’s spending just look terrible.

So I have a £300 / month “spend” on house improvements that smooths the outlay – all hypothetical of course.

LikeLike

Hi GFF – I think of my pots not as savings but as spends – and just annualise big expenditure –

Does that make sense ?

LikeLike

It does – but I’ve had some problems with reconciling say the purchase of a car vs. the spend.

What I’ve done is I saw that the car is worth what I paid for it, book it as an asset and depreciate it every month (2% roughly) and call that depreciation a cost/spend.

For home imrpovements (windows cost me £3k in Jan.) I book £X00 a month as “home” spend and allow that the hypothetically accrue before it is spent.

It’s maybe a bit messy but it gives a realistic impression of spending because 1) I can sell the car to get the money back 2) the cost for the house is there and needs to be done at some point so “saving/spending” for it now makes sense.

LikeLike

Helllo mate great blog post

LikeLike