One more month of squirreling, and what has it brought? Not as much as last month even though my savings rate is the same. My net work increased by…

- 0.43%

- £492

Nothing did very well this month, however one silver lining was I received my annual statement from my DB pension. I googled the transfer value and it is £273,106 (the calculator gives a range and I take the lower number), which is £35,023 increase from last year. Yippee!

Actions from last month

- Reinvest the RMG dividend due in Sept

- Update: done, the princely sum of £37

- Increase investing and reduce saving. Invest the £225 of the £250 I usually save

- Update: done, from this month I am starting investing a total of £670 into Vanguard Lifestrategy 80% Equity per month instead of £445

- Monitor my spending to see if I can increase my savings and investment

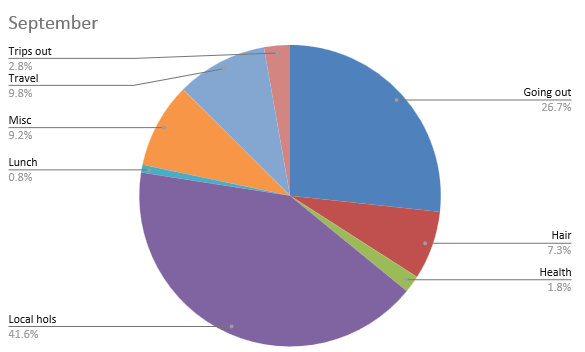

- Update: this was a bit of a surprise, I did monitor my spending quite diligently. I am a fan of cash but to help me monitor my spending I used my debit card 95% of the time. Bearing in mind, this expenditure is purely my personal money for eating out, drinks with friends, clothes, weekends way etc, and came to £831.11 – with £200 on eating out and drinks down the pub. I did though have some exceptional one off expenses

- nearly £300 on a 5 day cycle holiday in Scotland

- £75 on a handmade woollen cape for my nephews wedding

- Update: this was a bit of a surprise, I did monitor my spending quite diligently. I am a fan of cash but to help me monitor my spending I used my debit card 95% of the time. Bearing in mind, this expenditure is purely my personal money for eating out, drinks with friends, clothes, weekends way etc, and came to £831.11 – with £200 on eating out and drinks down the pub. I did though have some exceptional one off expenses

In the end there was very little money left over in September to invest, however it did motivate me see if I can manage my going drinking and eating, I do enjoy it but maybe a month every now and again, I challenge myself not to. Not October though, I have lots already in my diary!

Action for this month

Following on from the FIRE meet up in September I am planning on investigate the DC part of my pension and do some scenario-ising around using it as a bridge between when I want to FIRE and taking my DB pension – avoiding at least some of the penalties of taking by DC pension early. I may then have an action to increase my DC contribution in additional to or at the expenses of my S&S ISA.

Inspired by TEA’s post ‘That stuff is money…‘ I am committing to selling stuff on eBay during October. I don’t have anything major just some books and stuff so aiming for £60.

The suggestion to look at DC to bridge before you can take your DB is a good one. All of my pension is DC so I don’t have that to worry about. I do have a bridge before I can take DC, which I am ignoring at the moment and just planning to work until ~55. FI not FIRE!

All the best

-MM

LikeLike

To be honest Money Mage I think my goal is more FF – financial flexibility- where I work less / when I want and can cover basic expenses with investments – I can take my DB pension at 55 – but it’s has penalties – I may choose to live with them but each year I work adds £1000 pa – there is some modelling I need to do to be clearer about my options !

LikeLike

It’s fab that you are still adding to your DB pension, that’s the thing I miss most from my last employer! I clocked up some decent years before mine got frozen but the DC pension I’m paying into now is no comparison!

Good luck with the ebay selling – I have loads of stuff to sell but just can’t get round to it!

PS – 29th Nov is good for me.

LikeLike

I’ve clocked up

£10 on eBay (less

Fees) ! Not the windfall I imagined but good that stuff is getting a new home !

LikeLiked by 1 person